Top 5 articles, other good reads and a couple of TED Talks.

Please enjoy some of the articles that I read this month, starting with my top five:

My Money or Your Life

Despite increasing rates of obesity among industrialized countries, life expectancies have continued to rise. The biggest risk arising from the longer life expectancies is the extended payments that pensioners will receive. In America, defined benefit plans (aka pensions) have become far less common for those employed by private firms. However, government and municipal jobs continue to receive pension benefits. The IMF estimates that a life expectancy increase of one year adds $1 trillion to the world’s pension obligation.

Longevity Risk: My Money or Your Life, The Economist Magazine

How to be a millionaire and not even know it

This article is an interesting real life example of the issues discussed in the Economist article above. It is written by an advisor whose clients, both retiring teachers, were oblivious to the value of their pension benefits. “All my wife and I will get is a lousy pension” say the clients in a bit of fictitious dialogue. Their advisor does some math to show them that the present value of their pension is approximately $1.7 million. Let’s hope they weren’t math teachers.

How to be a millionaire and not even know it, by Marc Freedman, Money Magazine

Proof Negative

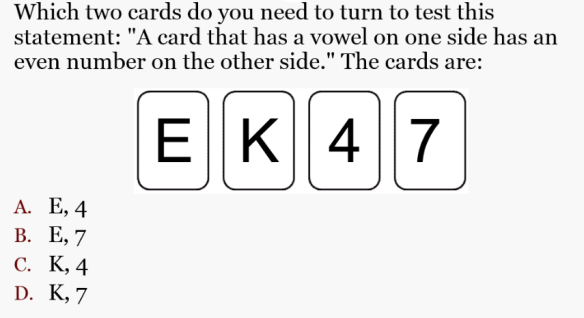

I love a good behavioral finance article. The author notes our natural inclination to seek evidence that confirms our previously held opinion. The greater point is that we tend to avoid or ignore evidence that proves us wrong. He gives an example:

The article states, “Most people answer with E and 4, but that’s wrong. For the posited statement to be true, the E card must have an even number on the other side of it and the 7 card must have a consonant on the other side. It doesn’t matter what’s on the other side of the 4 card. But we turn the 4 card over because we intuitively want confirming evidence. And we don’t think to turn over the 7 card because we tend not to look for disconfirming evidence, even when it would be “proof negative” that the given hypothesis is incorrect.”

It sounds right, but he left out a critical sentence from the original study, “subjects are aware that on the particular set of cards, each one has a letter on one side and a number on the other side.” The problem with this omission is noted by commenter “Neal” who points out that the K will also have to be turned over lest it also have a vowel on the other side.Here’s the beauty, after this is pointed out, instead of acknowledging his omission and the commenter’s correct point, says “You and Neal need to read the question more carefully.” Basically, when presented with disconfirming evidence, he dismissed it! He acted in the very behaviorially inefficient manner that he just described! Pure gold.

Proof Negative, by Bob Seawright, Above the Market blog

6 Behavioral Finance Principles Advisors Need to Know

Speaking of behavioral finance, this article lists six common behaviors. Among the list, I thought Selective Attention was particularly relevant. We find that misaligned expectations tends to be the biggest source of client dissatisfaction. As the article notes, “a lot of the time, we don’t even see what’s really out there in the world. Instead, we see what we’re looking for and what we expect.” We see this manifested during periods in which the S&P 500 or the Dow Jones Industrial Average, which represents “the market” according to the nightly news, outperforms other equity asset classes such as small cap, value of international stocks. A globally diversified portfolio is perceived to be underperforming “the market”.

6 Behavioral Finance Principles Advisors Need to Know, by Emily Zulz, Think Advisor

Practice makes imperfect

It’s a very appealing concept to believe that that harder work, greater talent and superior smarts will lead to success. In many areas of our lives and careers, that might be the case, but not in the case of mutual fund managers. The article cites a paper which examined 2,846 mutual funds between 1996 and 2008. The survival rate was abysmal: fewer than a quarter lasted more than five years and only 195 lasted a decade. Among those managers with superior performance, repeating their results proved challenging. In another study by Vanguard Funds, the funds that landed in the top 20% of performers were more likely to land in the bottom quintile than repeat their appearance in the top 20%.

The article notes our psychological inclination to seek active managers whom we believe will deliver superior performance. They refer to the Lake Wobegon effect in which everyone thinks they have the ability to select above average managers. The article accurately concludes that the quest for superior returns has, more often than not, led to excessive fees and disappointing returns.

Practice Make Imperfect, The Economist Magazine

Other good reads:

Finding an Identity Beyond the Workplace, New York Times

Has Indexing Gotten Too Big? Vanguard Funds

Do Optimists or Pessimists Manage Their Money Better? Yahoo Finance

5 Steps to Building a New Habit, Entrepreneur Magazine

A couple of good TED Talks:

The Transformative Power of Classical Music by Benjamin Zander

Measuring what makes life worthwhile, by Chip Conley