The Navigoe Blog

The Financial Quarterly: Q4 2023

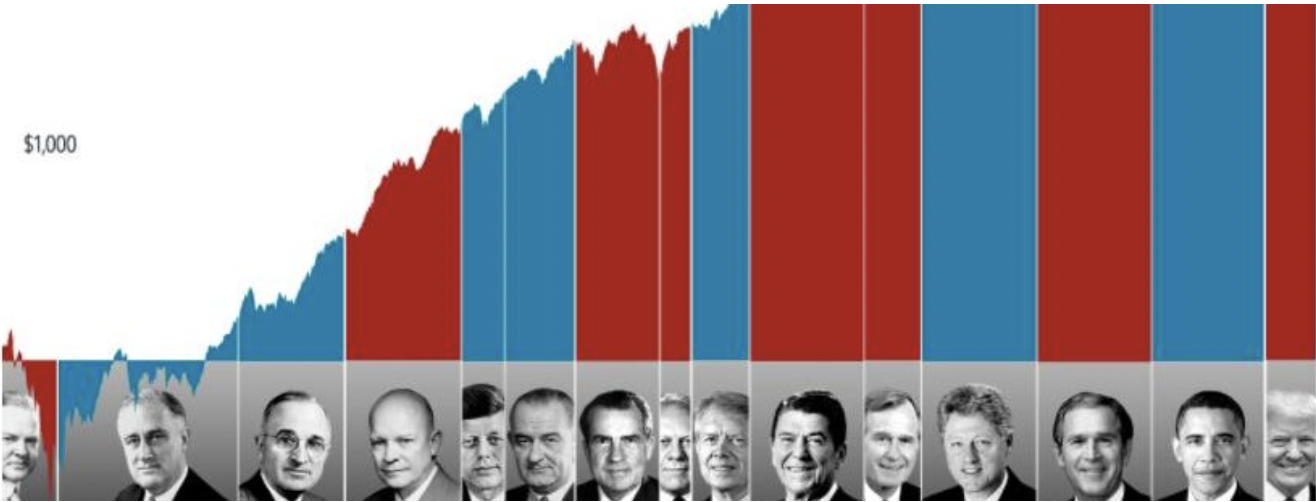

After a rocky year, stocks rallied in Q4 to end 2023 with a bang. Can we trust the bull market? Is a correction hiding around the corner? Will that predicted recession finally strike? Let’s discuss!

Happy Earth Day!

Happy Earth Day from the Navigoe Crew! This week we volunteered with South Bay Parkland Conservancy at Wilderness Park in Redondo Beach. We cleared space for new native plants to be planted today, in celebration of Earth Day!

Navigoe 2022 Q4 Market Review

We’re excited to present to you the latest in our quarterly webinar series featuring Navigoe Founder and CEO, Scott Leonard, and Dimensional Fund Advisor’s “Secretary of Explaining Stuff” Apollo Lupescu.

2022 Year End Letter to Clients

Dear Valued Client, Happy New Year! I hope that everyone was able to spend some quality time with the people that matter most this past holiday season. Before I get into the summary of last year, I want to share a quick story…

9 Key Principles to Improve Your Odds of Achieving Your Goals

Nine key principles that will help you improve your odds of achieving your financial goals.

A Review of the 2nd Quarter of 2022

We’re excited to present to you the latest in our quarterly webinar series featuring Navigoe Founder and CEO, Scott Leonard, and Dimensional Fund Advisor’s “Secretary of Explaining Stuff” Apollo Lupescu.

South Bay Magazine Profile

Navigoe had the honor of being profiled in South Bay Magazine for their special Financial Services section. For this profile, they interviewed our Founding Partner and CEO, Scott Leonard, about Navigoe’s services, what makes our firm unique, and what type of clients are typically best suited for our services.