Time to Stop Stock Picking: The Fundamentals Powering Modern Investment Management

For most of the investment industry’s history, success was positioned as an ability to pick the right stocks. Professional investors built careers around researching companies, identifying potential winners, and attempting to outperform the broader market through careful selection. Mutual funds and investment managers competed on their ability to find the next great company or avoid the next major decline.

This approach, known as active management, shaped how investors thought about portfolios for decades.

But over time, research and real-world results began to challenge the assumption that active management was the clear winning strategy. Many investors and academics started asking a different question: instead of trying to beat the market through individual stock selection, what if a more disciplined and diversified approach could produce better long-term outcomes?

At Navigoe, this shift in thinking has shaped how we approach portfolio construction and long-term investment.

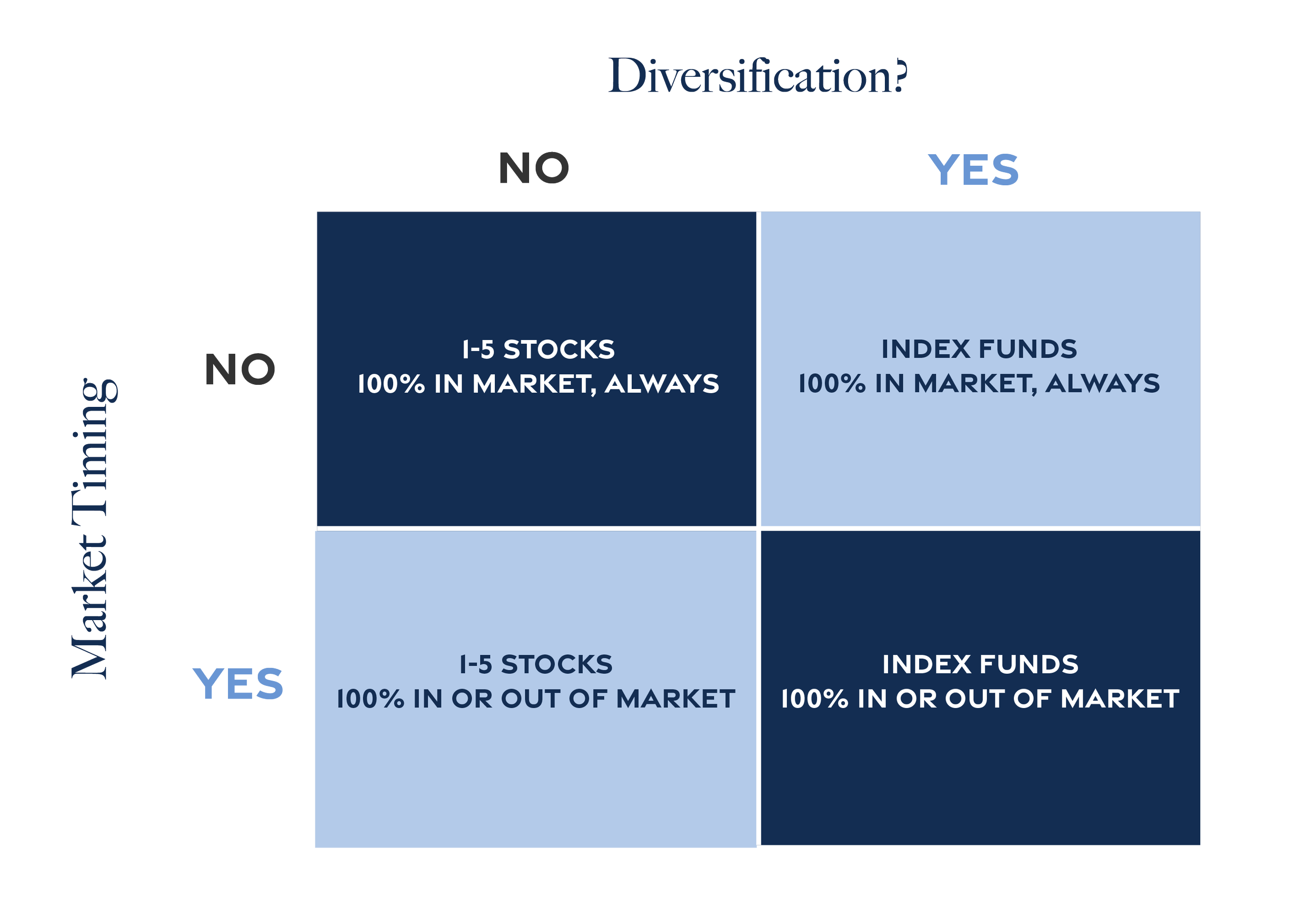

One helpful way to think about these approaches is through a simple framework that highlights the choices investors make when building a portfolio, hinging on your answer to two fundamental questions.

Is diversification important?

Is it possible to time the market successfully?

Depending on your responses, you have four possible approaches to investing, and each combination leads to a very different portfolio strategy.

You can think of it almost like a grid, with diversification on one axis and market timing on the other.

No diversification, no market timing: We often see this path as the long-term stock picker’s route. While you stay invested, you also stay concentrated. The belief is not that you can predict market moves, but you can identify a small group of companies worth owning over time.

Yes diversification, no market timing: This path typically involves using diversified, low-cost investment vehicles and staying invested rather than trying to predict short-term market movements. It’s also where many investors say they are philosophically aligned, even if their actions don’t always match.

No diversification, yes market timing: This path is one of the most concentrated and aggressive approaches. In practice, it often means owning a very small number of stocks and moving fully in or out of the market based on your outlook. If everything goes right, the upside can be significant, but the risks are equally high because the stock selection and market timing both have to work.

Yes diversification, yes market timing: While this approach can look more disciplined on the surface, timing decisions still drive the strategy. You may use index funds or other diversified investments, but still make ongoing calls about when to increase, reduce, or shift exposure. The portfolio is diversified, but the strategy still depends on short-term predictions.

Looking at the grid, it becomes clear that investors often hold conflicting expectations.

Many say they believe in diversification and that they don’t believe in market timing. But when they describe what they want from an advisor, the expectations often sound different. They may want someone to pick the winning stocks, avoid the underperformers, and get them out before markets fall.

In other words, the philosophy they describe and the outcomes they expect don’t always align.

That tension helps explain why active management remains so common.

What Is Modern Portfolio Theory?

The quadrant that combines diversification with avoiding market timing ultimately became the foundation of what is now known as Modern Portfolio Theory (MPT).

Modern Portfolio Theory focuses on two key ideas: diversification and avoiding market timing. Instead of trying to identify individual winning stocks or predict short-term market movements, the emphasis is on building a diversified portfolio and allowing markets to work over time.

Diversification reduces the impact that any single company, sector, or investment can have on a portfolio. If one holding performs poorly, the overall portfolio is less likely to suffer a significant decline.

At the same time, avoiding market timing removes the need to predict when to exit or reenter markets. As many investors have discovered, those decisions can be extremely difficult to make consistently.

Market timing requires two separate decisions: when to get out of the market and when to get back in. The moments when it feels safest to stay out of the market are often when uncertainty is highest and headlines are the most negative. Missing even relatively short periods of strong market performance can meaningfully affect long-term outcomes.

Rather than trying to outguess the market, this approach focuses on building a diversified portfolio, staying invested, and maintaining discipline through different market environments.

Active Management Versus Modern Portfolio Theory

Active management remains a common investment approach, but it can run against the logic of MPT in two ways.

First, active management often assumes someone can identify the right holdings ahead of time. But if that’s the advantage, then broad diversification can dilute the benefit of top stock selections.

Second, active management frequently involves some form of market timing, whether it’s explicit or not. Shifting exposures, making tactical allocation changes, or adjusting around expected market conditions are all timing decisions, even if they are framed differently.

But that doesn’t always mean every actively managed decision is automatically wrong. It does mean investors should understand the philosophy behind it and whether it actually matches their own.

For investors who want to follow an MPT-aligned approach, the practical implications are clear:

Use diversified investment vehicles, often index funds or similar structures.

Stay invested rather than trying to move in and out based on predictions.

Maintain a long-term allocation and rebalance it, rather than constantly adjusting in response to the latest market narrative.

While the framework itself is simple, maintaining that discipline can be difficult when markets become volatile or the headlines turn negative.

This is where guidance can play an important role. An advisor does more than just build a portfolio. They can help investors define their personal investment philosophy, understand the tradeoffs in their approach, and stay aligned with their strategy when uncertainty creates pressure to react.

If you want help articulating your personal investment philosophy or wish to review whether your current portfolio aligns with that strategy, schedule a meeting with Navigoe.